What is a Discretionary Family Trust?

A discretionary family trust is structure to hold assets in the name of an entity on behalf of family members.

A trustee is appointed to manage the trust and the assets are all registered in the trustee’s name and are held by the trustee on behalf of the beneficiaries. Rules for how the trust can operate are included in a written document called a trust deed.

The trustee has flexible powers to decide which beneficiaries will receive income and/or capital distributions each year.

A discretionary family trust may be useful for purposes such as asset protection, tax planning or estate planning. They can also provide benefits for family members who are unable to manage their own finances due to age, mental capacity or personal competencies.

How to set up a Discretionary Family Trust?

To set up a trust you need to work with a legal adviser to draft the trust deed and determine who will be potential beneficiaries and trustee.

There are some key roles and you should seek legal advice to decide who is best suited to fill each role:

- Settlor – makes the initial contribution to the trust

- Trustee – holds the assets on behalf of the beneficiaries and makes decisions including how to distribute income and/or capital

- Beneficiaries – are able to receive benefits from the trust

- Appointer – can remove the trustee and appoint a new trustee

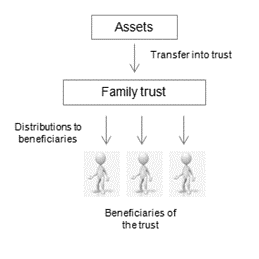

Assets can be transferred into the discretionary family trust. This will be a deemed disposal of the assets by the person transferring in the assets, and capital gains tax may be payable by that person.

The assets are owned by the trustee on behalf of the beneficiaries of the trust. Income derived from the assets is paid to the trust and the trustee decides which beneficiaries will receive distributions of income and/or capital.

Assets held in a trust will not form part of your estate upon your death.

You should seek legal and taxation advice to ensure your trust is established correctly. The trust deed should be drafted by a legal adviser to meet your needs.

Advantages and Disadvantages of Family Trusts

A family trust may have the following advantages and disadvantages:

|

Advantages

|

Disadvantages

|

|---|---|

|

Flexibility to decide how to distribute income and capital each year

|

All taxable income must be distributed or penalty tax (at the highest marginal tax rate plus Medicare Levy) will apply

|

|

Separation of legal ownership which may help to provide asset protection

|

Losses cannot be passed onto beneficiaries to reduce personal tax liability

|

|

|

Costs will be incurred to set up and managed the trust

|

Assets held in a trust are not owned by any person. Instead they are held on behalf of all beneficiaries but with no fixed entitlements. This may provide protection against claims from events such as bankruptcy, divorce or legal claims. It may also provide protection for people who cannot manage their own finances. However, in some cases, the courts can overturn this principle and treat assets in a trust as if the person owned the assets directly. You should speak to your legal adviser to understand these risks.

Read our Estate Planning Guide here.

Taxation Rules

Generally income of a trust (including franking credits) is distributed to beneficiaries and is taxable in the hands of the beneficiary at their marginal tax rate. The trust will pay tax on any undistributed income at the highest marginal tax rate plus Medicare levy.

The trust must have its own Australian Business Number and Tax File number. Tax returns will need to be lodged each year, but if all income has been distributed the trust will not pay any tax.

The trustee can consider the circumstances of individual beneficiaries when making the distribution. This means that overall tax may be minimised by making distributions to beneficiaries on lower marginal tax rates.

If the trust sells assets that have been held for at least 12 months, a 50% discount on realised capital gains can be claimed by individual beneficiaries who receive this distributed gain.

You should seek taxation advice on how the income of a discretionary trust will be taxed and the optimal strategies for trust distributions each year.

If you are transferring assets to the trust this will be deemed to be a disposal for capital gains tax purposes and you may need to pay tax on realised capital gains. You should seek taxation advice for the impact on your situation.

Centrelink/Veterans’ Affairs (DVA) Rules

If you have any involvement in a family trust (as trustee, appointer or beneficiary) Centrelink/DVA may deem you to be the ‘controller’ of the trust.

If you are deemed to be the controller (or a close family member is the controller) the value of assets in the trust will be included as an assessable asset in your assets test assessment.

Included in your income test will be the taxable income of the trust in the same proportion that you are deemed to own the assets. Who receives the distributions is irrelevant, however, if distributions are paid to someone other than the controller, Centrelink/DVA may consider this to be gifting. Amounts above the gifting limits will affect the controller’s income and assets tests assessment.

If you transfer money into a trust this may be assessed as asset and income to you for Centrelink/DVA purposes under the “source test”.

You should discuss your situation with Centrelink/DVA to determine the impact on your entitlements.

While a solicitor can take care of the legal aspects of your estate, at Progressive Financial Solutions, we can look at your total financial picture and help you with a broad range of issues such as funding and protecting your estate, avoiding challenges to your will, and minimising tax. You can read more about our Estate Planning Services here.